Retirement Plan Adds Up for this Single B.C. Woman, but New House not Part of the Equation

Selling her townhouse and buying a detached home with a basement suite for rental is beyond this 53-year-old’s means in this pricey market

Andrew Allentuck

Situation: At 53, woman with a good company pension and some savings wants to plan retirement

Solution: Add up future income streams to assess retirement readiness

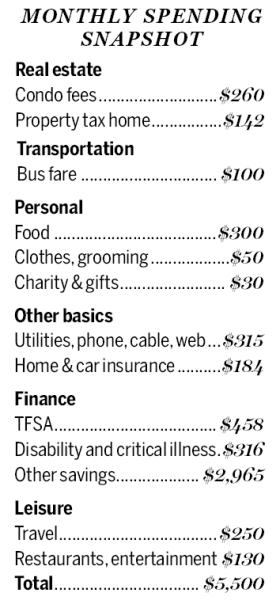

A woman we’ll call Valerie, 53, lives in the pricey Lower Mainland of B.C. A health-care professional, she brings home $5,000 net from her hospital job every month and rents out a suite in her home for $500 a month.

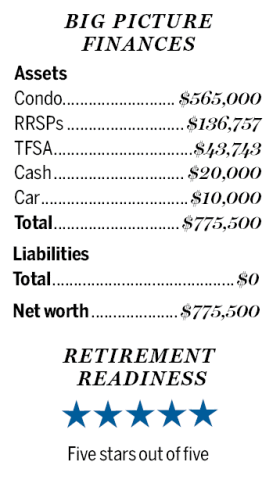

Valerie’s core issue is how to retire in perhaps seven years at age 60. She will have a solid pension from the hospital system in which she works. She has just over $200,000 in financial assets well invested, no debts, and a plan to hike and do charity work when she leaves her hospital and its stresses.

Her issues centre on predicting retirement income. “I want to ensure that I plan well for my future and at the same time enjoy life without financial struggle,†she explains. She has no children or spouse.

Pension Entitlements

Formerly a resident of a country in eastern Europe, she became a resident of Canada in 1991. With 26 years of residence to date, she can retire at 65 and thus qualify for 38/40ths of full Old Age Security, currently $6,942 per year. (Forty years of residence in Canada after age 18 are required for full OAS.)

Her Canada Pension Plan benefits will be about 80 per cent of the current $13,370 maximum at age 65. If she defers the start of CPP, she will get an 8.4 per cent boost for a maximum of five years or 42 per cent of the age 65 amount.

The question on every Toronto retiree’s mind: Do I sell my house now?

‘A case of career interrupted’: Hit with a layoff, couple’s reno plans and travel dreams looking iffy

In their mid-sixties and in a vise of debt, this B.C. couple needs a balance-sheet fix — and fast

Family Finance asked Derek Moran, head of Smarter Financial Planning Ltd. in Kelowna, B.C. to review Valerie’s choices.

“Her plans are a mix of wishes: For example, to sell her townhouse and buy a detached home with a basement suite for rental,†Moran says. “That’s not possible on her income in greater Vancouver, where she would like to be. Her pre-tax job income, including overtime, was $98,000 last year and her spending is just a third of that. If she remains frugal and does not make a huge commitment to a house that could jeopardize her financial independence, her retirement will be financially secure.â€

Income Components

The foundation of Valerie’s retirement will be a job pension. At 60, it would be $2,950 per month or $35,400 a year plus a bridge to 65 of $775 a month or $9,300 a year. At 65, the bridge vanishes and she is left with $35,400 a year. These are 2017 dollars. Indexing is not guaranteed.

Valerie’s RRSP, to which she has recently suspended contributions, has a present value of $136,757. If she works to age 60 and adds $10,000 this year to fill available space plus $5,000 each year for the next seven years to her age 60 and if she can obtain a 5 per cent return less 2 per cent for inflation, it will become $219,950 in 2017 dollars. If that money continues to grow at 3 per cent after inflation, and is spent over 30 years to age 90, it would support payouts of $10,900 a year in 2016 dollars.

Valerie’s TFSA has a present value of $43,743. If she adds $5,500 a year for the next seven years to her age 60, it will grow to $97,210. If that sum is spent over 30 years to her age 88, it would support tax-free distributions of $4,815 a year.

Adding up the numbers, from retirement at age 60 to age 65, Valerie would have the pension and bridge, total $44,700, $10,900 from her RRSP and $4,815 from her TFSA. She could add $6,000 in rental income. Her total, $66,415, taxed at an average rate of 20 per cent excluding TFSA payouts would leave her with $4,500 per month, well above present allocations of $2,077 a month with TFSA and other savings removed.

From 65 onward, Valerie would have her base pension of $35,400 a year, Canada Pension Plan benefits of an estimated $10,696 a year, Old Age Security of $6,595, RRSP payouts of $10,900 a year and TFSA payouts of $4,815 a year. Suite rent would add $6,000 for total cash flow before tax of about $74,400. She would not trip the OAS clawback which begins at about $73,000 because her TFSA payouts are not considered income. Thus her permanent retirement income would be $5,040 a month after 20 per cent tax based on age and pension credits and no tax on TFSA payouts.

Both before 65 and after, her income would more than maintain present spending net of savings. She could afford to postpone CPP to age 70. That would raise the payout by 42 per cent to $14,893 per year. Her OAS with a start delayed to 70 would pay about $8,970, all in 2017 dollars.

Valerie can also apply for the B.C. program of property tax deferral for seniors. For a present rate of 7/10ths of one per cent per year with no compounding, property taxes are deferred. It would save $1,750 per year at a cost of $12 per year. The tax deferred is repayable when the property is sold.

Timing Public Pensions

Whether to start CPP and OAS at 65 or to wait to 70 is a question of need for the money and life expectancy. If Valerie gets the money at 65 but does not spend it, she could make up some of the difference with investments. But the boosts of income of 42 per cent and 36 per cent are without risk and are indexed by the federal government. So those gains are very hard to match. There might be a loss to the clawback of some OAS benefit. With the income numbers above and a 15 per cent recovery tax on $1,500 of income, her clawback cost would be about $200 per year. The question of whether to take benefits at 65 or 70 depends, too, on life expectancy. If Valerie were to die before her mid-80s, postponement of benefits would have been the wrong choice.

“There is not much doubt that Valerie can have a secure retirement with ample income for her needs and a surplus for travel or other things and for contributions to good deeds such as the animal charities she favours,†Moran says.

(C) 2017 The Financial Post, Used by Permission