Couple has gone All-in on B.C. Real Estate, but a Secure Retirement will Mean Getting Out at the Right Time

Andrew Allentuck

Situation: B.C. couple betting on property market could be severely injured if interest rates rise

Solution: Cut leverage by selling rental property, diversifying assets, working at least to age 60

In British Columbia, a couple we’ll call Gerry, 29, and Ruth, 32, are thriving in their careers, his as a software manager in a large company, hers as a transportation network manager with a global business. They bring home $7,900 a month from their jobs, a good income in most parts of Canada but only middling in the expensive lower mainland where, in some areas, starter homes have seven-figure price tags.

To generate additional income, Gerry and Ruth rent out two suites in their home and rent out another property, which they bought by refinancing their first mortgage. Their goals are conventional — have children, pay off the mortgages, build up equity and retire in their early fifties — but achieving them will be a challenge.

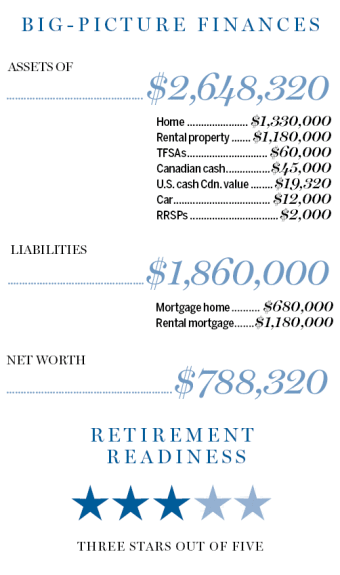

Their net rental income works out to $2,013 a month, giving them monthly disposable income of almost $10,000. That is ample for their present spending, but their margin of profit on their property is tied to interest rates, vacancy and costs and possible tenant damage. They are betting heavily on their real estate investments. Their present equity is $650,000, almost all due to appreciation in the hot B.C. market and a gift of $400,000 from their parents for a down payment on their home. The risk to their fortune is that property prices — now at nosebleed levels — could fall or their costs could rise.

“I want to continue purchasing rental properties and holding them so that after the mortgages are paid off in 25 to 30 years, we can pocket all the rental income,†Gerry says.

Family Finance asked Derek Moran, head of Smarter Financial Planning Ltd. of Kelowna, B.C., to work with Gerry and Ruth. He notes that the couple has made what amounts to a single big bet on B.C. real estate. All their investments, other than about $64,000 cash and $60,000 in TFSAs, are in residential B.C. property in their hometown. Their properties have appreciated a great deal, but their mortgages add up to $1.86 million, which is almost 20 years of the take-home income that backstops their rental sideline. “This undiversified portfolio could become hard to sell if the market turns,†Moran says. “So, add illiquidity to their risks.†Indeed, when markets fall, they can seize up and make trades all but impossible.

The Property Portfolio

The risks of their almost total real estate commitment are apparent in the math: Out of $55,200 in annual income from their rentals, they deduct $5,500 for property tax, $1,400 for insurance and $24,144 interest. That leaves $24,156, which is two per cent of the cost base of the $1,150,000 building.

Gerry and Ruth could try to increase the rents they charge to accommodate higher financing costs, but B.C. rent controls limit increases to 2.9 per cent a year. If interest rates do rise it is not likely that increasing their rents would be enough to offset all the higher carrying costs, Moran says.

Interest rates will rise one day. It could happen when rates begin to move up to historical norms or by lenders just increasing their margins. To avoid having to sell their rental unit or their house, each of which could rise in price at some time in future, they could draw on their cash. They have $45,000 in Canadian funds and about $19,320 in U.S. funds valued in Canadian dollars. If they keep $20,000 for emergencies, job loss, etc., they could use the balance — about $44,320 — for a lump sum payment on their $680,000 home mortgage. That payment would save $23,800 of interest and reduce amortization, now 22 years, by almost two years. That cuts their risk.

An alternative is to set a sell price on the rental unit, Moran suggests. If they can get a sufficient price, pay capital gains taxes and with what is left over, pay off their home mortgage, their risks would decline dramatically and they would be on their way to a financially stable retirement, he says.

Retirement planning

Investment income from the rental properties would be extra. To bring their income to $100,000 a year, diversified investments earning three per cent a year after inflation would need about $1,750,000 of capital. That would generate $52,500 and put them over the top. Ruth’s company does not provide any pension plan.

Retiring a decade or more before the earliest eligibility for CPP benefits implies that neither Ruth nor Gerry would earn full age-65 benefits. So we’ll estimate that Gerry and Ruth each pile up benefits worth 67 per cent of the 2016 maximum, $13,110. At age 65, which is three years apart for the couple, each would get $8,783. Also at 65, each would get Old Age Security of $6,846 in 2016 dollars. Starting each CPP plan at age 60 with a 36 per cent reduction in age 65 benefits would be a way to get through a few years of reduced income from investments. A strong property market rising at just two per cent per year would provide the capital base they need to push the present $1.2 million value of their rental property to $1.9 million, which would be more than enough to provide the income, combined with Gerry’s pension, sufficient to add up to $100,000 a year before tax, Moran says.

“Odds are that the couple will be able to achieve their goal of retirement in 20 years, but those odds will improve if they diversify their almost 100 per cent commitment to B.C. real estate,†Moran says. “Risks rise faster than potential returns. That’s the greatest downside to the couple’s plans."

(C) 2016 The Financial Post, Used by Permission