How this Couple with $4.58-million Net Worth Can Reduce the Clawback on Their Substantial Savings

Andrew Allentuck

Situation: Couple with pensions and hefty investments will be in clawback territory when RRIFs start to roll in

Solution: Make gifts in their lifetimes to their children, start paying out RRSP assets soon to average tax

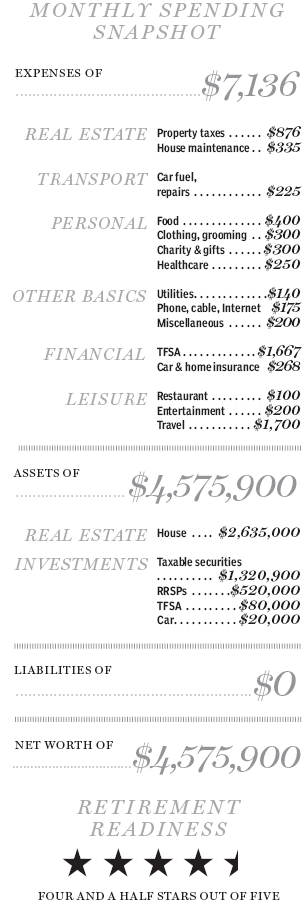

British Columbia has been good to homeowners who bought into the present property boom well before it started. That’s the good fortune a couple we’ll call Harry, 65, and Phyllis, 61, enjoy. With a combined net worth of about $4.58 million, 58 per cent of it their $2.635 million home, their problems are income and tax management.

Both have substantial job pensions from their former careers with big companies. Harry can expect $47,184 a year and Phyllis $24,120 a year, plus a bridge of $7,080 a year to 65. The sum of all pensions and investment income, Canada Pension Plan and Old Age Security benefits will ensure that their retirement income will not drop below $100,000 and will, after Phyllis turns 65, rise to almost $121,000 a year before tax.

“If we remain healthy, we’d like to stay in our house for another 15 to 20 years,†Phyllis says. “Rather than leaving money to our two children, each in their mid-20s, we’d like to assist them in purchasing homes when they are ready.â€

Family Finance asked Derek Moran, head of Smarter Financial Planning Ltd. in Kelowna, B.C., to work with Harry and Phyllis. His view – “they had the luck to buy a home when prices were less than 10 per cent of what they are today. They have worked and saved to a prosperous retirement.â€

The big picture of the couple’s finances is remarkably simple: $2.635 million in their house, $520,000 in RRSPs, $80,000 in tax-free savings accounts, $1,320,900 in taxable investments and $20,000 in their cars. They have no debts, so their net worth is $4,575,900.

The immediate need is to spend $100,000 for home renovations. They can take the money out of a $225,000 unregistered savings account. It earns little and they plan to stay in their home for many years.

When Phyllis should take CPP and OAS is an issue. Harry has already made the decision to take his government benefits — $8,844 for CPP each year and $6,778 for OAS — but Phyllis does not need either benefit now and so should wait to 65 for CPP. Neither will have income over the OAS clawback threshold of about $73,000 in 2015.

However, if she elects to defer OAS for five years, she can gain 7.2 per cent per year of her present $6,778 benefit. Looked at as an investment, that is a terrific return on a secure income asset. It’s like a government bond with an exceptional return. She will give up five years of benefits, a total of $33,890, but can gain that back and more if she lives beyond her mid-80s. Given that she does not need the money now, it’s a move well worth considering.

Tax Liability

Their success as savers will cause some grief when they have to start taking money out of their RRSPs. If their $520,000 of RRSPs is annuitized while growing at three per cent a year after inflation, they would generate taxable income of $27,100 in 2015 dollars for the 29 years to Phyllis’ age 90. Their taxable accounts, worth $1,320,900, with the same assumptions (but with a reduction of $100,000 for home improvements) would generate cash flow, including return of capital, of $63,627 a year.

Postponement of OAS benefits will help manage current taxes, Moran notes. If they do not act to reduce investment income, then, when their RRSPs are converted to RRIFs at age 71 with income flowing the next year, the sum of RRSP income ($27,100), investment income ($63,627), job pensions ($71,304), CPP benefits ($21,084) and two OAS benefits ($13,556), would give them total annual income of $196,670. Even with splits of eligible pension income, they would each face clawback tax at 15 per cent of sums over the threshold of about $73,000. That’s on top of the B.C. tax rate schedule that in 2015 can be as high as 45.8 per cent, though with care they can reduce it. To avoid high taxation, they can start tapping their RRSPs this year.

Harry and Phyllis will probably be unable to avoid clawback tax when their RRSPs begin to flow. But they can reduce the cost of the clawback by starting a gifting program for their two children. For each $100,000 reduction of capital paid out to the kids, using the annuity assumptions above, they would cut income by $5,060. If they give $300,000 to each child to assist in buying a home, the $600,000 reduction in their capital would reduce their income by $30,360 and reduce the cost of the clawback to about $1,525 each. That’s a 60 per cent reduction in the clawback. Call it a generosity “dividend,†this alternative deserves consideration, Moran says.

Portfolio Management

Harry and Phyllis need to address the efficiency and even the purpose of their investment portfolio. They have a remarkably high level of cash and cash-equivalent savings accounts, GICs and monthly income funds, amounting to 59 per cent of non-registered investments, 100 per cent of their RRSPs in GICs, some linked to stock market indices and 100 per cent of their TFSAs in GICs.

The case for hiring a professional portfolio manager at about 1 per cent of assets under management is compelling — the couple is barely pacing inflation before taxes on the trifling interest their $600,000 in GICs earns. Moreover, their approximately $800,000 of mutual fund monthly income funds have fees of up to 2.6 per cent. If they were to obtain another two per cent a year from their approximately $1.94 million in financial assets after payment of the one per cent management fee and restructuring of their investments out of costly mutual funds, their income would rise by $38,800, Moran explains.

The couple can also consider a variety of trust structures for their financial and other assets. If they put their taxable assets into a so-called Joint Partner Trust, the assets would not go through probate when the parents pass on. That would save probate fees of $14,000 per million of assets. Harry and Phyllis, as trustees, could retain control of the estate while alive and of sound mind and their children could take over at a later date. If they wait until Phyllis is 65, then, given the rule that both trustees by 65 or older, they can avoid a deemed disposition rule for assets transferred to the trust and resulting capital gains taxes. And, if the trust owns their home, the tax-free gain on the principal residence will continue.

The trust structure would entail legal fees to set it up and annual accounting fees. The biggest gain would be probate avoidance and a smooth transition of control upon or even prior to the death of the last partner.

Some tax planners suggest that life insurance be purchased to pay taxes on deemed disposition at death, but for older persons such as Harry and Phyllis, the cost could be substantial. The trust would eliminate the need for this kind of life insurance, Moran says.

“This couple has done a lot of things right and not too many things wrong,†Moran says. “If they raise their investment returns, reduce exposure to the clawback and deal with probate and other future costs when the last partner dies, they will have a five star retirement plan.â€

(C) 2015 The Financial Post, Used by Permission