OPTIMISM #16 - September 29, 2020

Dear clients and friends,I chopped the text below from a Norman Rothery column in the Globe and Mail last week called Making the Case for the sleepy approach to Dividend Investing. It’s the best description I have seen in a while of my own philosophy on investing. Enjoy.

Many speculators trade frequently, but investors should focus on the long term rather than on the short term. Smart investors like to buy and hold for very long periods while their firms grow and pay dividends.

Ask seasoned investors about their best purchases and they’ll often point to big gains from stocks they held for decades rather than from those they held for months or years. More than a few will point to the dividends they’re getting from long-held stocks that are now comparable to the cost of buying the stocks in the first place.

Such a sleepy approach works well when it comes to Canadian dividend stocks. The idea is to buy stocks with generous yields to build a diversified portfolio in a low-cost manner.

I recently highlighted research from professor Kenneth French at Dartmouth College on the returns of Canadian dividend stocks, and they’ve been superb in the past. Canadian stocks with the highest 30 per cent of yields gained an average of 14.1 per cent from the start of 1977 through to the start of 2020, while the market gained 10.2 per cent over the same period.

For peace of mind, I’d personally pick stocks with generous yields while avoiding those with extreme yields.

The sleepy approach to dividend investing holds a great deal of appeal.

I’ve been doing something similar with a part of my personal portfolio for a long time to good effect. (I own many of the stocks shown in the table.) Let us hope the approach will allow dividend investors to sleep well over the years while generating generous returns along the way.

Norman Rothery, PhD, CFA, is the founder of StingyInvestor.com.

--------------------------

I found this in a used book store one summer. Should have bought it.

Apple did go broke in the 1990s. Now it’s the most valuable company in the world.

It’s amazing how unpredictable the future can be.

____________________________________________________________________________________

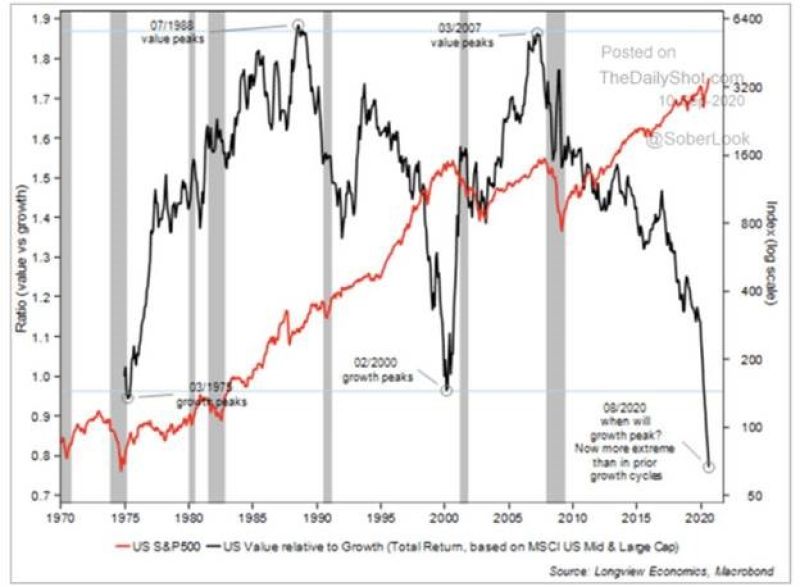

Growth stocks are generally expensive, with the idea that they will be worth much more in the future, justifying a higher than normal price today. Examples are Apple, Tesla, Amazon, Shopify etc. Value stocks are mature companies like banks and utilities, life insurance and telephone companies that don’t grow as quickly anymore. There are exceptions but our dividend payers tend to fall in the ‘value’ category.

This graph is a bit confusing at first, but it helps if you ignore the red (or green… sorry I can’t tell) line. The black line oscillates between high and low, relative to growth stocks.

Thanks to our friends at Guardian Capital for the graph.

The black line is at a 50-year low and that historically, value stocks have done extremely well following such a scenario. In the year 2000, just before the tech crash, and in 1975, before the crash of Nifty Fifty growth type stocks, the relationship between value and growth was similar to today. After the year 2000 and 1975, our dividend payers had a fantastic run. I am optimistic.

Have a great week,